Liabilities are the amounts of money the company owes to others. Think of liabilities as obligations — the company has an obligation to make payments on loans or mortgages or they risk damage to their credit and business. An asset can be cash or something that has monetary value such as inventory, furniture, equipment etc. while liabilities are debts that need to be paid in the future. For example, if you have a house then that is an asset for you but it is also a liability because it needs to be paid off in the future. On 10 January, Sam Enterprises sells merchandise for $10,000 cash and earns a profit of $1,000. As a result of this transaction, an asset (i.e., cash) increases by $10,000 while another asset ( i.e., merchandise) decreases by $9,000 (the original cost).

Components of the Basic Accounting Equation

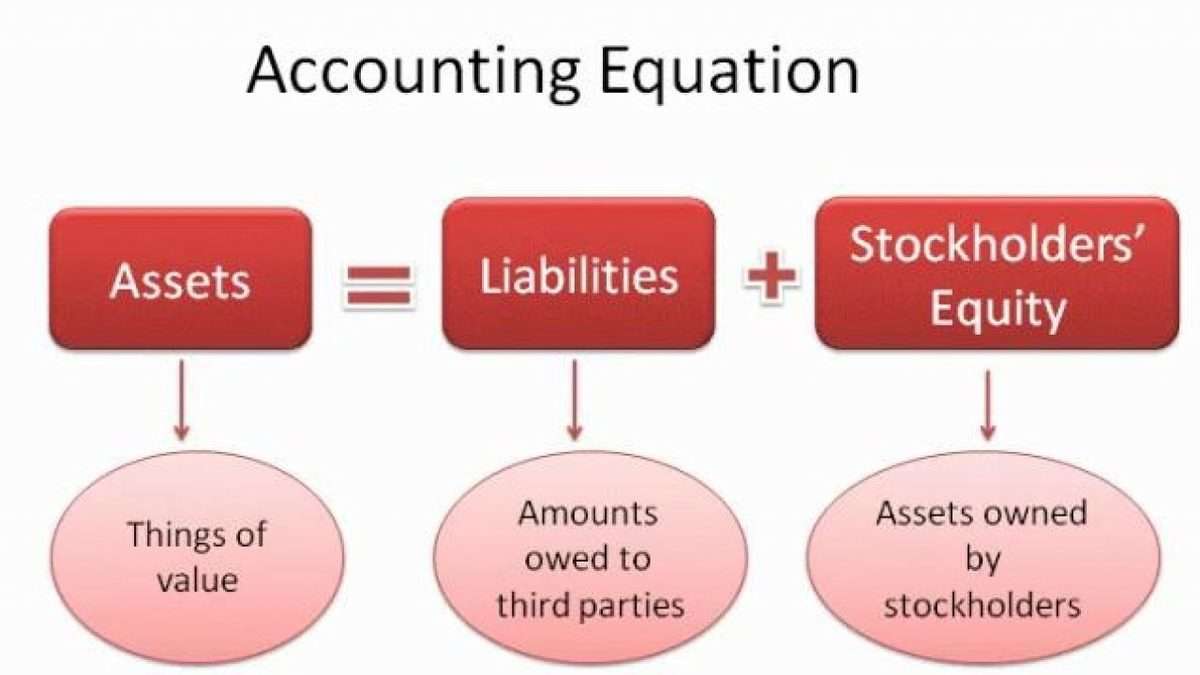

The claims to the assets owned by a business entity are primarily divided into two types – the claims of creditors and the claims of owner of the business. In accounting, the claims of creditors are referred to as liabilities and the claims of owner are referred to as owner’s equity. These may include loans, accounts payable, mortgages, deferred revenues, bond issues, warranties, and accrued expenses. Although the balance sheet always balances out, the accounting equation can’t tell investors how well a company is performing. Assets represent the valuable resources controlled by a company, while liabilities represent its obligations.

The relationship between the accounting equation and your balance sheet

While single-entry accounting can help you kickstart your bookkeeping knowledge, it’s a dated process that many other business owners, investors, and banks won’t rely on. That’s why you’re better off starting with double-entry bookkeeping, even if you don’t do much reporting beyond a standard profit and loss statement. Accountants and members of a company’s financial team are the primary users of the accounting equation. Understanding how to use the formula is a crucial skill for accountants because it’s a quick way to check the accuracy of transaction records .

Company

In its most basic form, the accounting equation shows what a company owns, what a company owes, and what stake the owners have in the business. These are the resources that the company has to use in the future like cash, accounts receivable, equipment, and land. The assets in the accounting equation are the resources that a company has available for its use, such as cash, accounts receivable, fixed assets, and inventory. Accounts receivable include all amounts billed to customers on credit that relate to the sale of goods or services. Inventory includes all raw materials, work-in-process, finished goods, merchandise, and consigned goods being offered for sale by third parties.

- Before technological advances came along for these growing businesses, bookkeepers were forced to manually manage their accounting (when single-entry accounting was the norm).

- For example, if the total liabilities of a business are $50K and the owner’s equity is $30K, then the total assets must equal $80K ($50K + $30K).

- It is used to transfer totals from books of prime entry into the nominal ledger.

- The accounting equation focuses on your balance sheet, which is a historical summary of your company, what you own, and what you owe.

Would you prefer to work with a financial professional remotely or in-person?

In worst-case scenarios, the company could go bankrupt as a result of mishandling finances using inaccurate numbers due to an unbalanced equation. The investment by the shareholders is structured as a share issue of 10,000 shares, issued at 5.00 each. The nominal (or par) value is 1.00, and the accounting rules require the par amount to be reported separately from the additional above par. The additional amount above par is reported in an account called additional paid-in capital or share premium. In order for the accounting equation to hold, Total Assets should ideally be equal to the sum of Total Liabilities and Total Equity.

It offers a quick, no-frills answer to keeping your assets versus liabilities in balance. In the above transaction, Assets increased as a result of the increase in Cash. At the same time, Capital increased due to the owner’s contribution. Remember that capital is increased the accounting equation is defined as: by contribution of owners and income, and is decreased by withdrawals and expenses. As business transactions take place, the values of the accounting elements change. This increases the cash account (Asset) by $120,000, and increases the capital stock (Equity) account.

Let’s take a look at the formation of a company to illustrate how the accounting equation works in a business situation. Equity represents the portion of company assets that shareholders or partners own. In other words, the shareholders or partners own the remainder of assets once all of the liabilities are paid off. However, due to the fact that accounting is kept on a historical basis, the equity is typically not the net worth of the organization. Often, a company may depreciate capital assets in 5–7 years, meaning that the assets will show on the books as less than their « real » value, or what they would be worth on the secondary market.

As you can see, no matter what the transaction is, the accounting equation will always balance because each transaction has a dual aspect. The accounting equation plays a significant role as the foundation of the double-entry bookkeeping system. The primary aim of the double-entry system is to keep track of debits and credits and ensure that the sum of these always matches up to the company assets, a calculation carried out by the accounting equation. It is based on the idea that each transaction has an equal effect.

In above example, we have observed the impact of twelve different transactions on accounting equation. Notice that each transaction changes the dollar value of at least one of the basic elements of equation (i.e., assets, liabilities and owner’s equity) but the equation as a whole does not lose its balance. Valid financial transactions always result in a balanced accounting equation which is the fundamental characteristic of double entry accounting (i.e., every debit has a corresponding credit). All assets owned by a business are acquired with the funds supplied either by creditors or by owner(s). In other words, we can say that the value of assets in a business is always equal to the sum of the value of liabilities and owner’s equity.