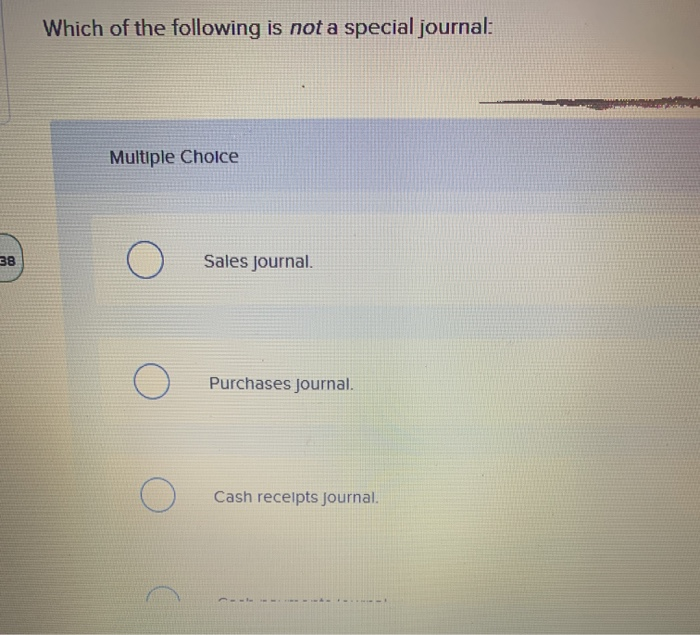

When a credit purchase is made, the company debits the goods purchased account and credits the accounts payable account in the purchases journal. When the accounts payable balance is paid off, the cash payment is recorded in the cash disbursements journal—not the purchases journal. Instead of having just one general journal, companies grouptransactions of the same kind together and record them inspecial journals rather than in the generaljournal.

How often should I update my purchases journal?

The sales journal will have only one column in which to enter the amount of each sales invoice. At the end of the month the total of the column is debited to Accounts Receivable and credited to Sales. Throughout the month, the individual sales invoices will be posted to each customer’s record found in the company’s subsidiary ledger for Accounts Receivable. At the end of the period, we would post the totals of $7,650 credit to cash, the $7,500 debit to accounts payable, and the $150 credit to merchandise inventory.

- There is also asingle column for the debit to Cost of Goods Sold and the credit toMerchandise Inventory, though again, we need to post to both ofthose.

- This may be daily, weekly, or monthly, depending on the type of business you run and the products and services you offer.

- The sales journal is used to record sales on account (meaning sales on credit or credit sale).

- Another difference is that the perpetualmethod will include freight charges in the Inventory account, whilethe periodic method will have a special Freight-in account thatwill be added when Cost of Goods Sold will be computed.

Subsidiary Ledger Fraud6

Forexample, a $100 sale with $10 additional sales tax collected wouldbe recorded as a debit to Accounts Receivable for $110, a credit toSales for $100 and a credit to Sales Tax Payable for $10. For example, a $100 sale with $10 additional sales tax collected would be recorded as a debit to Accounts Receivable for $110, a credit to Sales for $100 and a credit to Sales Tax Payable for $10. Special journals (in the field of accounting) are specialized lists of financial transaction records which accountants call journal entries. In contrast to a general journal, each special journal records transactions of a specific type, such as sales or purchases. For example, when a company purchases merchandise from a vendor, and then in turn sells the merchandise to a customer, the purchase is recorded in one journal and the sale is recorded in another.

OpenStax

In the case of the type of sales is a journal that accountants can use to record all sales transactions on a credit basis. In general, the information stored in this keeping is a summary of the invoices that the company issues to customers, such as transaction dates, account numbers, customer names, invoice numbers, and sales amounts. This type of document has the same function as a purchase journal, which makes it easier to record high-volume transactions on the ledger. At the end of the month, the amount column in the journal is totaled, and this amount is posted as a debit in the general ledger purchases account. It is also posted as a credit in the general ledger accounts payable account.

For example, if we overpaid our electric bill,we could get a refund check in the mail. We would use the cashreceipts journal because we are receiving cash, but the creditwould be to our Utility Expense account. If you look at the examplein Figure 7.23, you see that there is no column for UtilityExpense, so how would it be recorded? We would use some genericcolumn title such as “other” to represent those cash transactionsin the subsidiary ledger though the specific accounts wouldactually be identified by account number in the special journal. Wewould look up the account number for Utility Expense and credit theaccount for the amount of the check.

Internal Control and Special Journals

Match each of the transactions in the right column with theappropriate journal from the left column. Match each of the transactions in the right column with the appropriate journal from the left column. My Accounting Course is a world-class educational resource developed by experts to simplify accounting, finance, & investment analysis topics, so students and professionals can learn and propel their careers. Examples of such entries are adjusting entries, closing entries, transferring entries, and correcting entries.

Accounting information systems were paper based until the introduction of the computer, so special journals were widely used. When accountants used a paper system, they had to write the same number in multiple places and thus could make a mistake. Now that most businesses use digital do i have to file taxes in multiple states technology, the step of posting to journals is performed by the accounting software. The transactions themselves end up on transaction files rather than in paper journals, but companies still print or make available on the screen something that closely resembles the journals.

What other questions can be answered through the analysis ofinformation gathered by the accounting information system? An accounting information system should provide theinformation needed for a business to meet its goals. This journal should record non-routine transactions, and many of these transactions should be approved by the head of the accounting department or by someone with similar authority. One journal records similar transactions, which simplifies future references to any of them. Special journals allow the recoding of numerous repetitive transactions in one journal in one line.