Break-even analysis looks at internal costs and revenues, but doesn’t factor in external influences that can impact your business. — e.g., changes in market demand, economic conditions, inflation, supply chain disruptions, etc. For instance, if shipping costs rise due to global supply chain problems, your variable costs might go up and can throw off your original calculation.

Grade & GPA Calculators

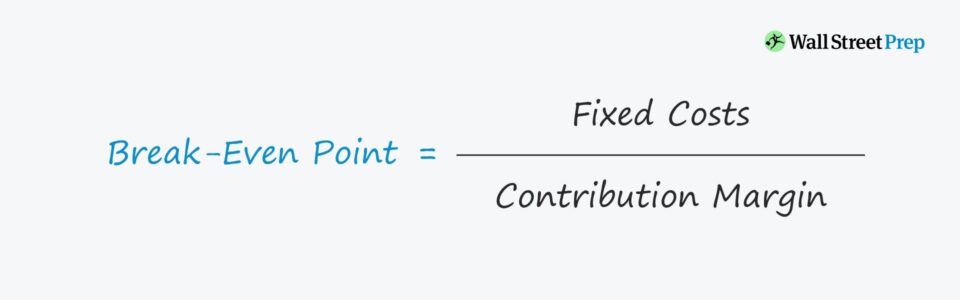

In other words, your company is neither making money nor losing it. The break-even formula can be adjusted to calculate the number of units that must be sold to reach a specific amount of profit. Fixed costs are any non-fluctuating costs that you pay on a regular basis, such as monthly or yearly. These are the same regardless of how many items you sell and include things like rent and business insurance. For corporate finance professionals, mastering the break-even point can be a game-changer.

Why apply the contribution margin formula?

Fixed Costs – Fixed costs are ones that typically do not change, or change only slightly. Examples of fixed costs for a business are monthly utility expenses and rent. The break-even point allows a company to know when it, or one of its products, will start to be profitable. If a business’s revenue is below the break-even point, then the company is operating at a loss. This gives you the number of units you need to sell to cover your costs per month.

Accounting Services

Finally, the breakeven analysis often ignores qualitative factors such as market competition, customer satisfaction, and product quality. While the breakeven point focuses on financial metrics, successful business decisions also require a holistic view that looks outside the number. For example, it may just not be feasible to sell 10,000 units given the current market for the example above. Let’s say that we have a company that sells products priced at $20.00 per unit, so revenue will be equal to the number of units sold multiplied by the $20.00 price tag. It may also help you determine whether you need to take cost-saving measures to try and achieve the same quality at a reduced price.

Importance of Break-Even Point Analysis

Dividing the fixed costs by the contribution margin will reveal how many units are needed to break even. Break-even analysis is great for entrepreneurs or companies that are just starting out and unsure of what to sell, how much to sell, or where to allocate their budget. This simple analysis can help that decision-making process by determining three golden rules of accounting examples pdf quiz more . how much product you’ll need to sell to be profitable and how long that product will last. You can adjust variables, fixed costs, sales price, and volume metrics in each analysis to determine how much to budget for each of those costs. When those fixed costs are subtracted, that will leave the company with $40,000 profit.

- In conclusion, just like the output for the goal seek approach in Excel, the implied units needed to be sold for the company to break even come out to 5k.

- This computes the total number of units that must be sold in order for the company to generate enough revenues to cover all of its expenses.

- If your price is too high, you might be falling short of your break-even point because customers won’t buy at that price.

Shape Calculators

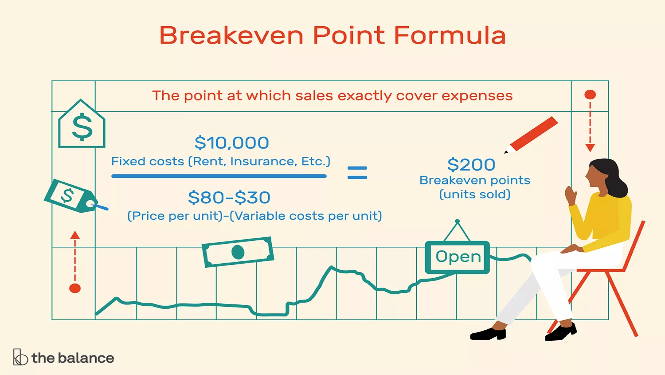

First we need to calculate the break-even point per unit, so we will divide the $500,000 of fixed costs by the $200 contribution margin per unit ($500 – $300). Upon selling 500 units, the payment of all fixed costs is complete, and the company will report a net profit or loss of $0. The break-even point is the volume of activity at which a company’s total revenue equals the sum of all variable and fixed costs.

If the price stays right at $110, they are at the BEP because they are not making or losing anything. Options can help investors who are holding a losing stock position using the option repair strategy. In conclusion, just like the output for the goal seek approach in Excel, the implied units needed to be sold for the company to break even come out to 5k. The incremental revenue beyond the break-even point (BEP) contributes toward the accumulation of more profits for the company.

Let’s take a look at how cutting costs can impact your break-even point. Say your variable costs decrease to $10 per unit, and your fixed costs and sales price per unit stay the same. In this example, the business needs to generate \($50,000\) in sales revenue to cover both fixed and variable costs and reach the break-even point. To find your variable costs per unit, start by finding your total cost of goods sold in a month. If you have any other costs tied to the products you sell—like payments to a contractor to complete a job—add them to your cost of goods sold to find your total variable costs. The denominator of the equation, price minus variable costs, is called the contribution margin.

The formula for calculating the break-even point (BEP) involves taking the total fixed costs and dividing the amount by the contribution margin per unit. A break-even analysis helps business owners find the point at which their total costs and total revenue are equal, also known as the break-even point in accounting. This lets them know how much product they need to sell to cover the cost of doing business.